Biden slams Republicans who oppose student loan relief but voted for tax cuts for the rich

Forty-three million Americans owe money on federal student loans.

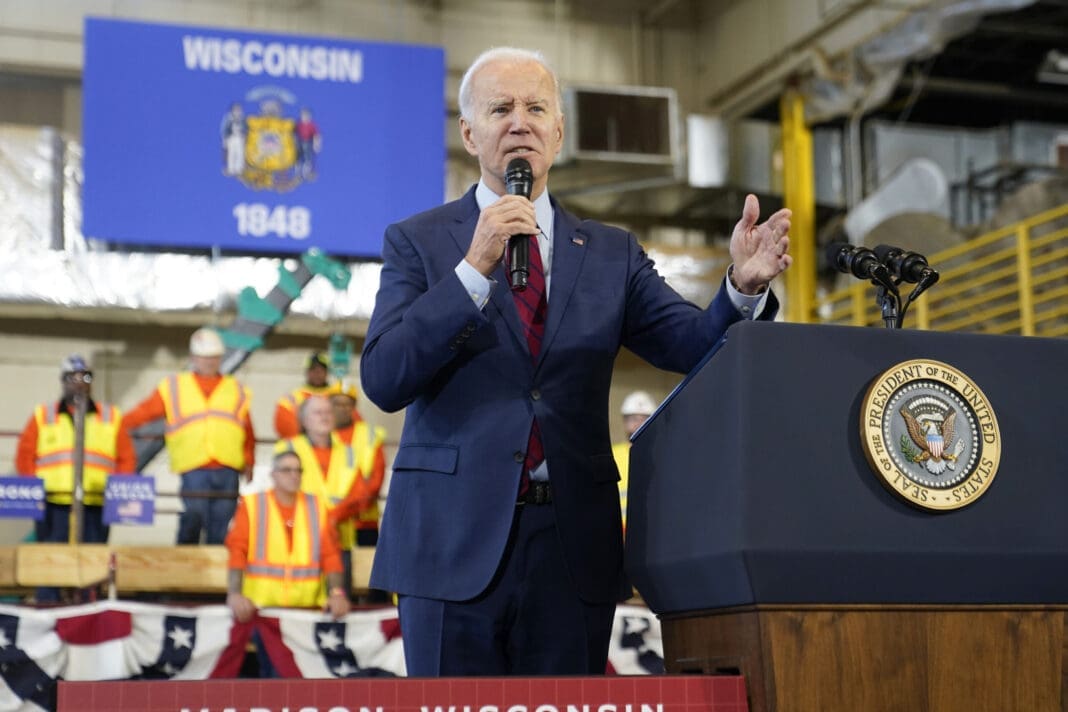

President Joe Biden, who on Aug. 24 announced a plan to cancel student loan debt for millions of Americans, criticized Republicans’ attacks on the plan, comparing his action with their support for massive tax cuts for the wealthy during Donald Trump’s presidency.

Speaking from the White House, Biden laid out the details of his plan, which would relieve $10,000 in student loan debt, or $20,000 for those with Pell Grants, federal aid provided to those with greater financial need:

I will never apologize for helping working Americans and middle class, especially not to the same folks who voted for a $2 trillion tax cut that mainly benefited the wealthiest Americans and the biggest corporations, that slowed the economy — didn’t do a hell of a lot for economic growth — and wasn’t paid for, and racked up this enormous deficit, just as we’ve never apologized when the federal government forgave almost every single cent of over $700 billion in loans to hundreds of thousands of small businesses across America during the pandemic. No one complained that those loans caused inflation. A lot of these folks and small businesses are working in middle-class families. They needed help. It was the right thing to do. So the outrage over helping working people with student loans I think is just simply wrong, dead wrong.

The relief offered by the Biden administration is only available to borrowers who earn less than $125,000, or $250,000 for married couples. The AP noted that 43 million people have federal student loan debt. In its statement on the plan, the White House said that the Department of Education was proposing a repayment plan for current and future low-income borrowers that will cap monthly payments for undergraduate loans to 5% of their discretionary income.

Polling has shown public support for Biden’s plan. A poll conducted Aug. 19-21 by Data for Progress finds that 60% of registered voters believed that the federal government should eliminate all or some student loan debt for all borrowers; sorted by party, the results in favor of canceling student debt are 81% of Democrats, 52% of independents, and 45% of Republicans.

Republicans, including some of the wealthiest members of Congress, with net worths reportedly in the hundreds of millions of dollars, lashed out at the plan.

Senate Minority Leader Mitch McConnell, whose net worth is reportedly over $30 million, described the plan as “student loan socialism” and “a wildly unfair redistribution of wealth toward higher-earning people.”

Sen. Rick Scott of Florida, who is worth over $200 million and is the wealthiest member of Congress from either party, complained, “@JoeBiden is putting hard working Americans, millions who didn’t attend college and/or have no debt, on the hook for $344 BILLION to pay other people’s bills.”

“Sad to see what’s being done to bribe the voters,” wrote Sen. Mitt Romney of Utah. “Biden’s student loan forgiveness plan may win Democrats some votes, but it fuels inflation, foots taxpayers with other people’s financial obligations, is unfair to those who paid their own way & creates irresponsible expectations.” Romney is worth at least $85 million, earned during his time leading Bain Capital, a private equity firm that reportedly laid off blue-collar workers at companies after taking them over.

Sen. Ron Johnson (R-WI) said the debt forgiveness was “grossly unfair” and that “Democrats have become the party of the elite.” According to his most recent Senate disclosures, Johnson’s assets are worth between $16.55 and $78.3 million.

Sen. Tom Cotton (R-AR) claimed the plan is a “bailout,” while Sen. Marsha Blackburn (R-TN) argued that it is a “gift to the rich.”

Most of the senators slamming Biden’s student loan plan voted in 2017 for the Tax Cuts and Jobs Act, signed into law by former President Donald Trump. That law contained tax cuts that disproportionately benefited the wealthy and cut taxes for large corporations. A study published by the Center for American Progress in December 2019 concluded: “It has been two full years since Congress passed the TCJA, and it is increasingly clear that the bill will not live up to its proponents’ exaggerated promises. Indeed, the tax cut has accomplished much less and cost much more than its proponents promised.

“Based on previously debunked economic theory, the bill will reduce revenues by trillions of dollars over the decade. So far, the large corporate tax windfalls have gone mostly toward lining the pockets of already wealthy individuals, and there is little evidence that middle- and working-class families will see real benefits.”

The Tax Cuts and Jobs Act ultimately contributed to a massive increase in the federal deficit during Trump’s time in office. An analyst with the Urban-Brookings Tax Policy Center told the Washington Post that the deficit growth under Trump was the third-largest in U.S. history, with the national debt increasing by $7.8 trillion.

On Monday, the Biden administration announced that it forecast this fiscal year’s budget deficit would be $400 billion lower than it had estimated in March. The drop in the deficit will be $1.7 trillion for the full year, it says, down to $1.03 trillion.

Published with permission of The American Independent Foundation.

Recommended

Biden calls for expanded child tax credit, taxes on wealthy in $7.2 trillion budget plan

President Joe Biden released his budget request for the upcoming fiscal year Monday, calling on Congress to stick to the spending agreement brokered last year and to revamp tax laws so that the “wealthy pay their fair share.”

By Jennifer Shutt, States Newsroom - March 11, 2024

December jobs report: Wages up, hiring steady as job market ends year strong

Friday’s jobs data showed a strong, resilient U.S. labor market with wages outpacing inflation — welcome news for Americans hoping to have more purchasing power in 2024.

By Casey Quinlan - January 05, 2024

Biden’s infrastructure law is boosting Nevada’s economy. Sam Brown opposed it.

The Nevada Republican U.S. Senate hopeful also spoke out against a rail project projected to create thousands of union jobs

By Jesse Valentine - November 15, 2023