43 GOP senators back House Republicans' cuts-or-debt-default threat

Enough Senate Republicans to filibuster legislation say they will not back any clean debt limit increase.

As the United States stands just weeks away from a possible catastrophic default on its national debt, most Senate Republicans say they will oppose any effort to raise the debt ceiling unless it is paired with draconian spending cuts.

On Saturday, Sen. Mike Lee (R-UT) and all but six of the 49 lawmakers in the Senate Republican caucus sent to Democratic Senate Majority Leader Chuck Schumer endorsing efforts by the House Republican majority to tie any debt ceiling increase to a significant reduction in federal spending:

The Senate Republican conference is united behind the House Republican conference in support of spending cuts and structural budget reform as a starting point for negotiations on the debt ceiling.

Our economy is in free fall due to unsustainable fiscal policies. This trajectory must be addressed with fiscal reforms. Moreover, recent Treasury projections have reinforced the urgency of addressing the debt ceiling. The House has taken a responsible first step in coming to the table with their proposals. It is imperative that the president now do the same.

As such, we will not be voting for cloture on any bill that raises the debt ceiling without substantive spending and budget reforms.

Cloture is a procedural vote in the Senate to end filibusters over legislation. If 41 signatories make good on their threat, they could successfully filibuster a debt ceiling bill and block any action.

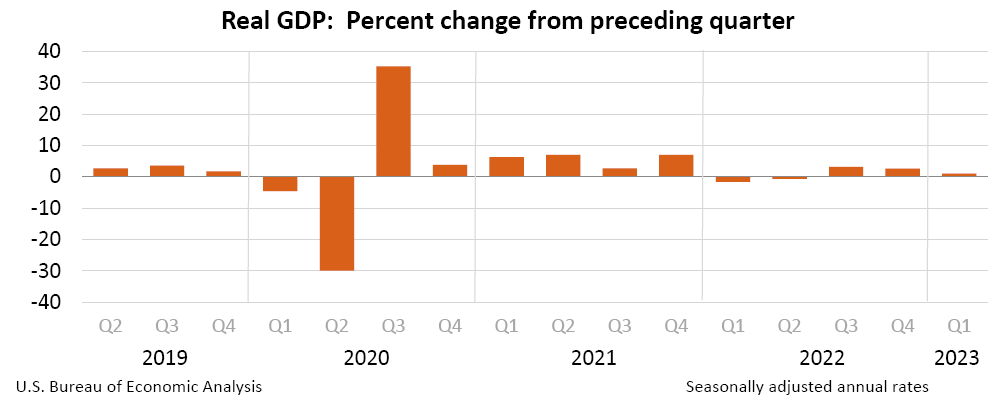

Contrary to the Republican senators’ claim that the U.S. economy is in free fall, the real gross domestic product has increased in each of the last three quarters and in seven of the nine quarters since President Joe Biden took office, according to the U.S. Bureau of Economic Analysis.

On May 5, the Bureau of Labor Statistics reported that the economy added 253,000 jobs in April, bringing the unemployment rate down to 3.4%, tied for the lowest rate since 1969.

By law, the U.S. Treasury Department can borrow no more than $31.381 trillion to pay for operations or interest on the loans it has already taken out. Unless this cap is raised, Treasury Secretary Janet Yellen said, the government will be unable to pay for its spending obligations starting at the beginning of June. Experts warn that a debt default would be catastrophic for the world’s economy.

The U.S. has incurred $31 trillion in national debt over decades, thanks to spending approved by Democratic and Republican lawmakers. About a quarter of it was accumulated during former President Donald Trump’s four years in the White House.

Biden and congressional Democrats proposed a one-time no-strings-attached increase in the debt ceiling and separate negotiations over the budget.

House Republicans refused, instead passing a bill that would pair a $1.5 trillion debt ceiling increase with $4.5 trillion in federal spending cuts over a decade, including repeal of investments in clean energy and measures to combat climate change, cuts in funding of the Internal Revenue Service as it works to crack down on wealthy tax evaders, and an estimated 22% cut in all discretionary spending.

These cuts would likely hurt older Americans, veterans, and everyone who relies on the government for benefits and programs. It would likely cost thousands of announced jobs.

The GOP bill also contains rollbacks of environmental regulations, new impediments to wind energy development, and language that would make it easier for oil and gas companies to build pipelines and drill on public lands.

The president is scheduled to meet on Tuesday with Schumer (D-NY), Senate Minority Leader Mitch McConnell, House Speaker Kevin McCarthy, and House Minority Leader Hakeem Jeffries in an effort to resolve the impasse.

While the United States has never defaulted on its debts, congressional Republicans in recent years have used the debt ceiling as a bargaining chip to force policy concessions.

In 2011, even the threat of a possible default was enough to spook credit rating agencies. Standard & Poor’s lowered the nation’s long-term debt rating from AAA to its current AA rating, making it more expensive for the Treasury Department to borrow money, and the delays increased the government’s borrowing costs by about $1.3 billion in that fiscal year, according to a 2012 Government Accountability Office report.

While it is not yet clear what damage the current fight is causing to the nation’s credit rating, Yellen warned in a May 1 letter, “If Congress fails to increase the debt limit, it would cause severe hardship to American families, harm our global leadership position, and raise questions about our ability to defend our national security interests.”

According to the Treasury Department and Congressional Budget Office, a default would likely cost 500,000 Americans their jobs and shrink the economy by 0.6%.

Published with permission of The American Independent Foundation.

Recommended

Biden calls for expanded child tax credit, taxes on wealthy in $7.2 trillion budget plan

President Joe Biden released his budget request for the upcoming fiscal year Monday, calling on Congress to stick to the spending agreement brokered last year and to revamp tax laws so that the “wealthy pay their fair share.”

By Jennifer Shutt, States Newsroom - March 11, 2024

December jobs report: Wages up, hiring steady as job market ends year strong

Friday’s jobs data showed a strong, resilient U.S. labor market with wages outpacing inflation — welcome news for Americans hoping to have more purchasing power in 2024.

By Casey Quinlan - January 05, 2024

Biden’s infrastructure law is boosting Nevada’s economy. Sam Brown opposed it.

The Nevada Republican U.S. Senate hopeful also spoke out against a rail project projected to create thousands of union jobs

By Jesse Valentine - November 15, 2023

{kind=link}